Help

Darren Krett

Monday 20 February 2023

Volume & Open Interest

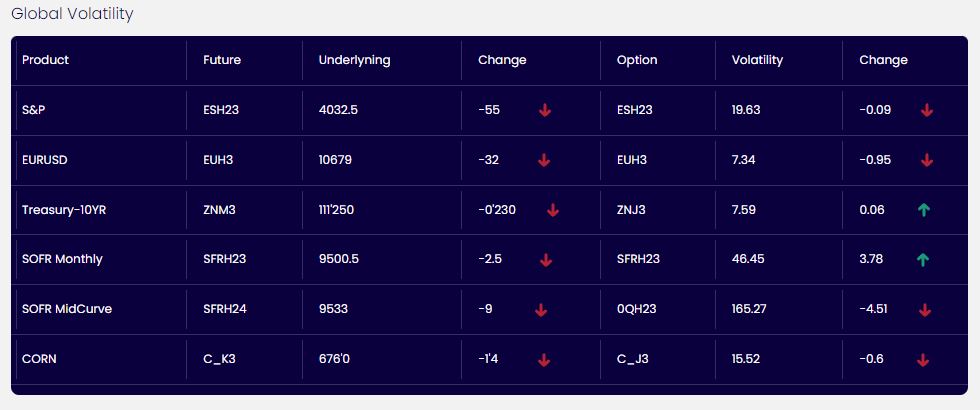

The Volume and Open Interest page (Vol/OI) is a very useful tool in analyzing where Open Interest is targeting, whether it is adding or decr

Volume & Open Interest

0

Comments (0)

Darren Krett

Tuesday 21 February 2023

Share on:

Post views: 11012

Categories

Blog

Stocks have returned from the long weekend in the red tracking European peers while there have been several key US earnings updates with both Walmart (WMT) and Home Depot (HD) opening lower after weak guidance.

There has also been attention on geopolitics after US President Biden's visit to Ukraine on Monday. Data saw EU PMI data miss on manufacturing but with strong services metrics, helping support the composite above expectations while in the UK PMI data beat across the board. The US PMI beat across the board and only extended pressure to stocks with the economy showing great signs of resilience despite all the Fed tightening seen so far while commentary on pricing was also hawkish. The January Existing home sales data cooled 0.7% M/M to 4.000mln, beneath the expected rise to 4.1mln. Sectors opened predominantly in the red with underperformance seen in consumer discretionary after the aforementioned earnings, while Real Estate and Utilities also lag. On the flip side, Energy is the only sector trading in positive territory despite mixed performance in energy benchmarks.

Elsewhere, the Dollar is at highs and above 104.00 after the latest PMI data while Treasuries are lower across the curve. Looking ahead, US President Biden is speaking in Poland & ECB's Lagarde is speaking on Finnish TV.

Darren Krett

Monday 20 February 2023

0

Comments (0)

Darren Krett

Wednesday 2 November 2022

0

Comments (0)