STOCKS, FUTURES AND OPTIONS END OF DAY REPORT MAY 5th

HIGHLIGHTS

The White House is reportedly weighing a short-term extension of the debt ceiling to allow parties to keep negotiating, according to CNBC

FED’s BULLARD said in an event in Minneapolis he thought the 25bps hike this week was a good step, but there is a lot of inflation in the economy. Implying that may be where we are heading is closer to 5.50-5.75%,given his buoyant commentary on the economy and dismissive attitude towards any banking issues, but then he followed that by saying that he is ready to be data-dependent, and was open minded on whether to pause or hike at the June meeting, so maybe he does have one eye on them after all and then with another lovely pirouette he said he does think that ultimately, rates are going to have to grind higher.

US bank deposits fell to USD 17.167tln from 17.180tln in prior week, according to Fed data Bank credit at all US commercial banks rises to USD 17.37tln vs 17.32tln in prior week.

UK conservatives lose over 1,000 councillors in ‘hammering’ as Labour becomes largest local government, according to Sky.

Regional banks skyrocketed, with shorts covering in fear of any regulatory intervention over the weekend.

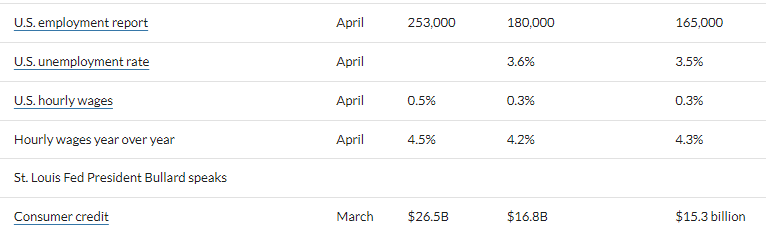

And of course, with YET ANOTHER MISS TO THE UPSIDE, with have the US Non-Farm Payrolls 253k vs. expected 180k

SUMMARY

Stocks rallied through the session on Friday with banking short sellers getting squeezed in fear of regulatory intervention, while a hot NFP report was indicative of a stubbornly hot labor market - helped the markets surgew higher although it should be noted that they were (SPX and NDX) were still lower on the week.

Ecen though there was no new news for the banking sector, the regional banks surged, with the KRE ETF up 6%, and PacWest surging 82%. This is what is called a "mass short-covering", with traders not wanting to take the risk of some sort of regulatory intervention over the weekend.

There was also good news from Apple which was nearly up 5%.

And then, of course we had yet another miss to the upside with today's strong NFP number and coupled with a pretty strong hourly earnings( up+0.5% MM),things seem more in line with the Fed's rhetoric, even though the market still believes that the Fed will have to cut by year end and then later on Fed’s Bullard (non-voter) said he was “even open to a pause in June”, which was like throwing fuel onto the fire and helped stocks rally throughout the day, with the S&P looking to possibly have another charge at the 4214 range high next week? Bullard’s comments also helped stopped the bashing the Treasuries were getting too.